📊 Key Data Snapshot (May 2026)

HD Price: ~$322 | 52-Week Range: $310 – $427

FY2025 Revenue: $164.7B (+3.2% YoY) | Full-Year Comp Sales: +0.3%

FY2026 Guidance: +2.5% to +4.5% revenue growth

Analyst Consensus: Buy | Avg Target ~$424 | Forward P/E: 22.16x

A housing slowdown that isn’t going away

Home Depot has always been one of the clearest barometers of the US housing market. When homes change hands, people renovate. When construction picks up, contractors spend. For years, that cycle drove the company’s growth. But right now, that cycle is stuck.

Housing turnover has remained at historical lows since 2023. Homeowners who locked in sub-3% mortgage rates during the pandemic aren’t moving — and why would they? The combination of elevated rates and home prices still significantly above 2019 levels has essentially frozen a large segment of the market. Fewer transactions means fewer renovation triggers, and that hits Home Depot right where it hurts most: big-ticket spending on kitchens, bathrooms, and full renovation projects.

CEO Ted Decker acknowledged it plainly in the FY2025 earnings call: “Ongoing consumer uncertainty and pressure in housing defined the year.” That’s management-speak for: things are still tough, and we’re not expecting a quick recovery.

What the numbers actually say

For all of FY2025, Home Depot reported $164.7 billion in revenue — up 3.2% year-over-year on the surface. But the headline figure is misleading if you don’t look underneath it. Comparable sales — the true measure of organic demand at existing stores — grew just 0.3% for the full year. Net earnings declined 4.4% to $14.15 billion. Diluted EPS fell from $14.91 to $14.23.

Q4 told a similar story. Sales came in at $38.2 billion, down 3.8% from the prior year. Q4 comp sales edged up only 0.4%. The roofing segment was particularly rough — industry shipments dropped 28% year-over-year in Q4, the lowest volume since 2019.

“Adjusting for storms, underlying demand was relatively stable throughout the year.” — CEO Ted Decker, FY2025 earnings call

Management’s framing is fair — storm activity does create volatility in roofing and repair categories. But “stable” is a long way from “growing,” and the market knows it. HD stock is trading near its 52-week low as a result.

The SRS acquisition: the biggest story most people are missing

Here’s what often gets left out of HD analysis: in mid-2024, Home Depot completed the largest acquisition in its history — an $18.25 billion deal to acquire SRS Distribution, a leading specialty trade distribution company serving professional contractors in roofing, landscaping, and pool construction.

This matters enormously. SRS gives Home Depot access to markets it previously couldn’t serve well — large-scale specialty contractors who don’t shop in retail stores. Through SRS, the company gained a distribution network, deeper penetration into the professional trade supply chain, and entirely new revenue categories.

In FY2025, SRS delivered low single-digit organic sales growth despite the difficult environment. For FY2026, management is targeting mid-single-digit organic growth from SRS, with 40 to 50 new SRS locations planned. That’s a meaningful growth engine running alongside the traditional retail business — and one that is structurally less sensitive to DIY consumer softness.

The PRO strategy: less DIY, more contractor

Beyond SRS, Home Depot has been systematically building its PRO segment — serving contractors, builders, roofers, and landscapers — as a counterweight to the weaker consumer environment. Professional contractors spend more consistently, buy in larger volumes, and keep working even when the housing market is soft.

Home Depot has invested in dedicated PRO sales teams, extended credit facilities, supply chain upgrades, and the SRS platform to serve this segment. The pivot from a primarily DIY retail model to a hybrid retail-plus-trade-distribution business is arguably the most important strategic shift the company has made in a decade.

The tariff risk you cannot ignore

Any HD analysis written in 2026 that ignores tariff exposure is not complete. Home Depot sources a significant portion of its products internationally, including from China and Mexico — both directly impacted by current US trade policy.

Elevated tariffs create cost pressures on imported goods, squeeze gross margins, and add uncertainty for consumers already cautious about spending. Analysts covering HD have flagged tariff exposure as a near-term headwind. Management’s FY2026 gross margin guidance of approximately 33.1% suggests they believe they can manage through it — but this is a live variable, not a settled question.

The macro chain that drives everything

Elevated inflation → High Fed rates → Expensive mortgages → Frozen housing market → Reduced renovation demand → Pressure on HD sales

The good news is this chain runs in reverse too. If the Fed begins a meaningful easing cycle, mortgage affordability improves, housing turnover recovers, renovation demand rebounds — and Home Depot captures outsized demand on the other side. Management’s FY2026 guidance implies they are not counting on a rate cut windfall, but positioning for a patient, gradual recovery.

HD vs Lowe’s: who has the edge right now?

Home Depot has historically skewed more toward the PRO contractor, while Lowe’s tilts toward the DIY consumer. In the current environment — where PRO demand is holding up better than DIY — HD’s positioning is actually working in its favor. The SRS acquisition extends that edge further. Lowe’s has no equivalent specialty trade distribution platform.

On valuation, HD trades at a forward P/E of 22.16x, below its one-year median of 23.77x. That compressed multiple reflects the market pricing in near-term uncertainty — but also creates a potential entry point for investors who believe the cycle will eventually turn.

Three scenarios to watch

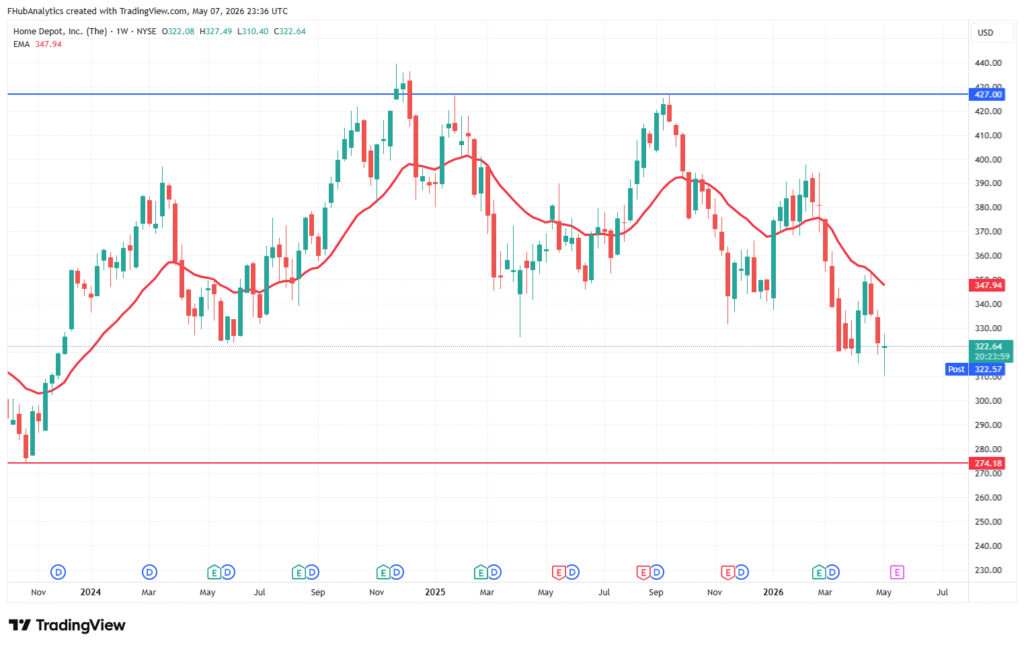

Bear case: Rates stay elevated, housing remains frozen, comp sales go flat or negative. HD breaks below the $310 immediate support level — the next meaningful floor on the chart sits at $274, which would represent a further 13% decline from current levels. That is the level to watch if $310 fails to hold.

Base case: Gradual recovery in line with management guidance. HD trades in the $310 to $380 range while investors wait for macro clarity. The EMA at ~$348 acts as the key dynamic resistance to reclaim on the upside.

Bull case: The Fed begins cutting rates in H2 2026, SRS outperforms expectations, and housing turnover starts to recover. HD reclaims the EMA, breaks above $380, and re-rates toward the $420 to $430 analyst target range — in line with the $427 resistance visible on the weekly chart.

What to keep on your watchlist

Technical levels: Immediate support at $310 (52-week low). Secondary support at $274 — the next major floor if $310 breaks. EMA resistance currently at ~$348 and sloping downward. Base case range $310–$380. Analyst consensus target ~$424, aligning with the $427 resistance on the weekly chart.

Key catalysts to monitor: Fed rate cut decisions and their impact on mortgage rates. Monthly housing starts data — a sustained recovery above 1.4 million units would be bullish. SRS organic sales growth vs the mid-single-digit management target. Quarterly comp sales direction — a return to +2% or above signals demand recovery. Tariff policy developments affecting import costs and margins.

Bottom line

Home Depot is navigating one of the tougher macro environments it has faced in years. The housing market is soft, big-ticket renovation demand is weak, and tariff uncertainty adds an extra layer of near-term risk. None of that is new news — and the stock price near its 52-week low reflects it.

What the market may be underpricing is the structural transformation underway. SRS gives HD a growth engine that doesn’t depend on the housing cycle. The PRO segment provides stability when DIY consumers pull back. And HD’s market leadership — scale, supply chain, and pricing power — means it is better positioned than most to wait out a prolonged downturn.

For patient investors, HD at ~$316 — trading below its historical P/E average — represents a bet not on the current environment, but on the eventual turn. That turn will come. The question, as always, is when.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Analysis is based on publicly available information as of May 2026. Investing involves risk, including the potential loss of capital. Readers should conduct their own research before making any investment decisions. Fremora Analytics Hub does not provide personalized investment advice.